Autor: Shelby Benavidez

In March 2025, the Financial Crimes Enforcement Network (FinCEN) made a dramatic change to the way corporate ownership transparency works in the United States. Under a new interim final rule, most U.S.-based companies no longer have to report their “beneficial owners” — the individuals who ultimately own or control the company — to the federal government. This change is a big shift away from the rules set by the Corporate Transparency Act (CTA), which was created to fight money laundering, terrorism funding, and other illegal money activities by making company ownership clearer.

The change has sparked a sharp divide. Business advocates are celebrating the reduction in regulatory burden, while transparency advocates warn it could weaken financial crime enforcement. This article explains what the change is, why it happened, and what its implications may be for the future.

Background on U.S. Beneficial Ownership Reporting Rules

Corporate Transparency Act: Key Requirements and Purpose

The Corporate Transparency Act, passed in 2021, was part of the U.S. government’s effort to stop hidden shell companies. A shell company is a business that exists mostly on paper, with little or no real operations or employees, and they often hide who really owns or controls them. Before this law, it was difficult for law enforcement to find out who actually owned companies involved in illegal activities. The Corporate Transparency Act required “reporting companies” to disclose their beneficial owners to FinCEN, creating a confidential federal database that could be accessed by law enforcement and certain financial institutions. The law required “reporting companies” to disclose their beneficial owners to FinCEN, creating a confidential federal database that could be accessed by law enforcement and certain financial institutions.

Under the original rules, most corporations, limited liability companies (LLCs), and similar entities formed or registered to do business in the United States had to report this information. The only entities exempt from reporting were certain regulated businesses, large operating companies with substantial U.S. operations, and some nonprofit organizations.

What Counts as Beneficial Ownership Information (BOI)?

Beneficial ownership information refers to the details of the individuals who, directly or indirectly, either own at least 25 percent of the company’s equity interests or exercise substantial control over the company, such as senior officers or key decision-makers. This data includes each beneficial owner’s full legal name, date of birth, current residential or business address, and an identifying number from an official document such as a passport or driver’s license.

The CTA’s intention was not to make this information public. Instead, the information would be stored in a secure database available to law enforcement and other authorized entities, primarily for the purpose of combating financial crimes.

Why Beneficial Ownership Reporting Faced Opposition

Even though the CTA aimed to stop criminals from misusing companies, many small business owners and trade groups strongly opposed the reporting rule. They said it created a lot of extra paperwork, especially for small businesses that don’t have legal or compliance staff to handle it. Others worried about privacy because they had to share personal ID documents with the government. Some also pointed out that the new rule overlapped with other reporting requirements, since some businesses already had to share ownership information with state agencies or banks. These concerns helped lead to the big change announced in March 2025.

FinCEN’s 2025 Rule Ending Most BOI Reporting Requirements

March 2025 FinCEN Change to Beneficial Ownership Rules

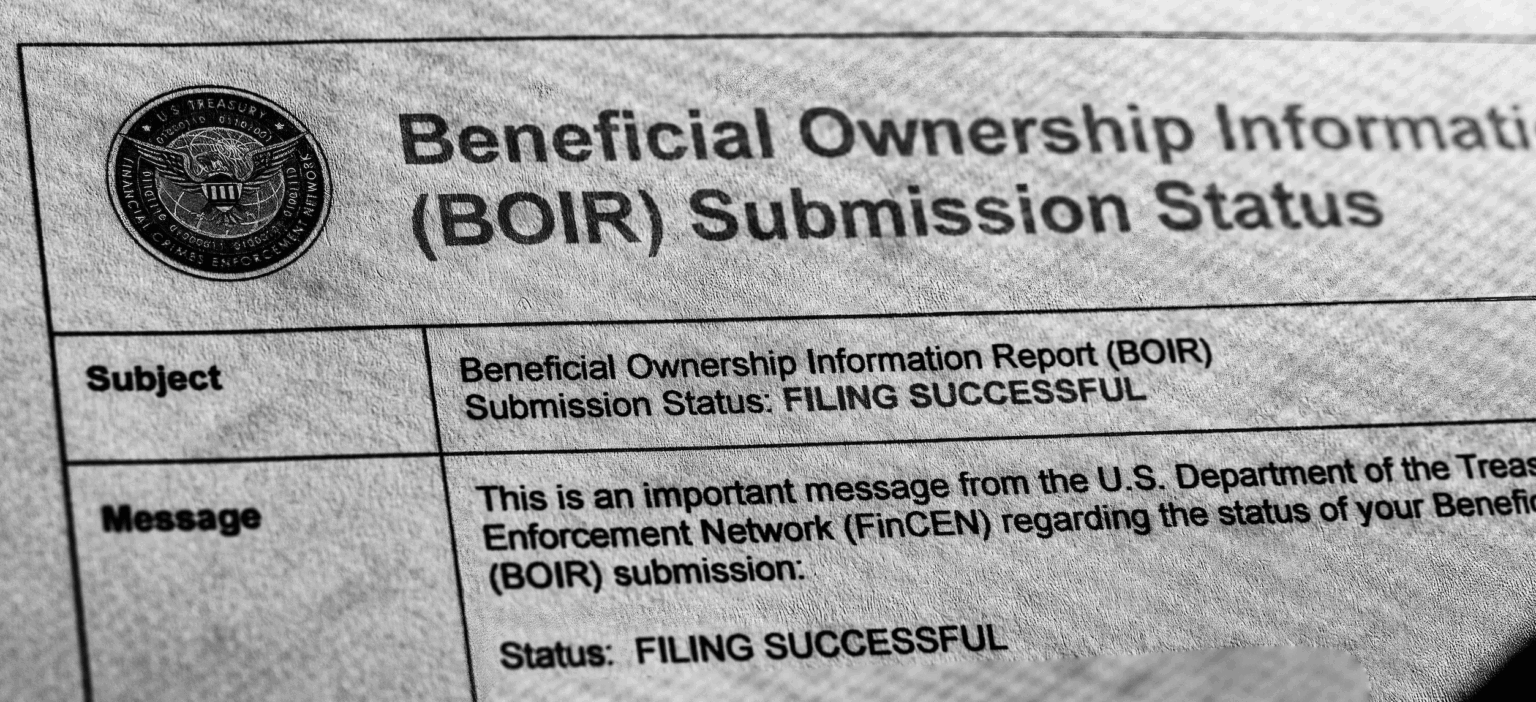

On March 21, 2025, FinCEN announced — and on March 26 officially published — an interim final rule removing the BOI reporting requirement for all domestic companies, meaning any entity formed in the United States. The rule also exempts U.S. citizens and residents from having to report their ownership of foreign entities. As a result, the vast majority of businesses that were previously obligated to file BOI reports are now exempt from doing so.

According to FinCEN’s own estimates, the change reduces the number of affected companies from around 32 million to roughly 20,000. This is a reduction of more than 99 percent, leaving only a small fraction of entities still subject to the requirement.

Who Must Still Report Beneficial Ownership to FinCEN

The new rule retains the reporting requirement for foreign entities that register to do business in the United States. However, even these companies are no longer required to report any U.S. individuals who are beneficial owners. In other words, the scope of reporting is now limited to foreign corporations, limited liability companies, and similar entities that have registered with a U.S. state or tribal authority, and only with respect to their non-U.S. beneficial owners. The vast network of domestic businesses and their owners has been entirely removed from the BOI reporting system.

2025 Deadlines for Foreign Entities Filing BOI Reports

For the small number of companies that still have to report beneficial ownership, there are two important deadlines. Foreign companies registered before March 26, 2025, must file their ownership information with FinCEN by April 25, 2025. Companies that register on or after March 26, 2025, have 30 days from their registration date to submit the information. These shorter deadlines match the smaller group of companies that now need to report.

Implications and Reactions

Why Some Businesses Support Ending BOI Reporting

Supporters of the new rule, including many small business advocacy groups, argue that it lifts an unnecessary and costly administrative burden from millions of U.S. companies. They contend that the original reporting requirements would have consumed time and resources that small businesses simply cannot spare, particularly those without dedicated compliance teams. Proponents also highlight the privacy benefits of eliminating the requirement to share sensitive personal identification data with a federal agency. In their view, the change prevents the duplication of reporting obligations for businesses that are already disclosing ownership details to state-level authorities or financial institutions. Organizations like the National Federation of Independent Business (NFIB) have described the rollback as a major victory for the small business community.

Why Critics Oppose Ending Beneficial Ownership Reporting

Critics see the situation very differently. Many transparency advocates argue that removing BOI reporting for domestic companies undermines the core intent of the Corporate Transparency Act. They warn that the rollback could open the door for criminals to exploit U.S.-based shell companies to conceal illicit funds or conduct unlawful transactions. Law enforcement agencies, which had anticipated using the database as a powerful investigative tool, will now face challenges in tracking beneficial ownership across jurisdictions. Some policy experts also worry about the broader implications for U.S. credibility on the global stage. Over the past decade, the United States has urged other countries to adopt beneficial ownership transparency measures, and this policy reversal may be perceived as a retreat from that commitment.

What’s Next for Beneficial Ownership Rules in the U.S.

The new rule is classified as an interim final rule, meaning it takes effect immediately but remains open to public comment. FinCEN is expected to review these comments and could issue a final rule later in 2025. Opponents of the change may also challenge it in court, particularly if they believe it conflicts with the statutory language or purpose of the Corporate Transparency Act. Until then, U.S. law enforcement agencies will need to adjust to operating without a comprehensive beneficial ownership database for domestic companies. Internationally, policymakers will be watching closely to see whether this rollback influences other countries’ willingness to maintain or adopt similar transparency requirements.

FinCEN’s decision to remove beneficial ownership reporting requirements for U.S. companies represents one of the most significant rollbacks in the short history of the Corporate Transparency Act. For supporters, it is a long-overdue relief from regulatory red tape, sparing millions of businesses from a complex and potentially invasive compliance process. For critics, it is a setback in the fight against illicit finance, one that may weaken the ability of law enforcement to uncover hidden ownership structures. Whether the benefits to business outweigh the potential costs to financial transparency remains an open question — one that will likely dominate policy discussions, and perhaps legal challenges, in the months ahead.